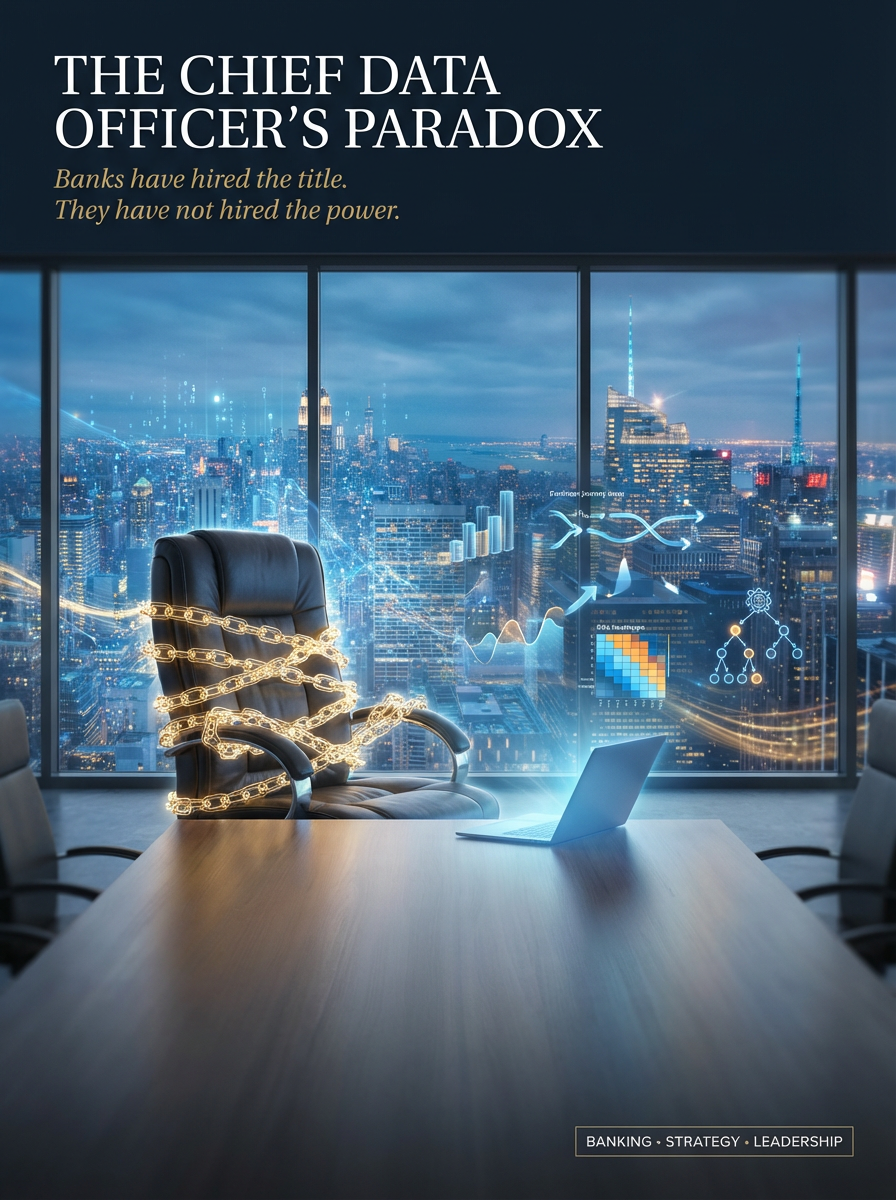

The Chief Data Officer’s Paradox

Banks worldwide have hired the title. They have not hired the power. That asymmetry is about to cost them.

The Two Boardrooms

Two boardrooms. Two capitals. The same week.

In the first, a newly appointed Chief Data Officer walks in with a deck worthy of the job description: a governance framework in crisp diagrams, a five-year cloud roadmap, a color-coded matrix of regulatory obligations. The CEO nods. The CFO approves the budget. The Chairman moves on.

Six months later, the CDO is still waiting on architectural sign-offs stalled between three committees. He reports to the CTO, so every cross-functional conversation begins and ends as a negotiation about IT priorities. He is managing a function. He is not shaping a bank.

In the second, a different CDO walks into a quarterly strategy session with no deck at all. He brings a single finding: the bank is quietly bleeding its most profitable clients to a competitor that has learned to personalize wealth advisory at scale. He shows, transaction by transaction, where the institution is blind.

Within two weeks, a cross-functional task force reports to him. Within three months, a customer intelligence platform is in production. Within two years, the bank has rewired its commercial logic around data-driven segmentation.

Same title. Same pay grade. Two entirely different banks.

The difference is neither talent nor technology nor budget. It is empowerment: the gap between being hired to manage data and being trusted to reshape how the institution thinks. Most banks have appointed a CDO. Few have empowered one. In an era when Open Banking, generative AI, and digital-native competitors are rewriting the economics of financial services, that gap has stopped being an HR matter. It has become existential.

IDEA IN BRIEF

The Problem. The CDO title has spread across global banking faster than the authority required to make it matter. Most CDOs govern data and satisfy regulators. Few are trusted to redesign how the bank competes.

The Argument. An empowered CDO, reporting to the CEO or Board with real budget authority, cross-functional decision rights, and cultural license to challenge legacy practice, becomes a catalyst for enterprise reinvention rather than an expensive compliance officer.

The Payoff. Six compounding shifts: reporting to revenue, reactive to predictive risk, AI ambition to AI readiness, product silos to customer integration, cost center to operational alpha, talent scarcity to talent magnetism.

What “Empowered” Actually Means

Empowerment is not a feeling. It is a structure. In banking, it resolves across five specific dimensions. Miss one, and the role collapses into ceremony.

The reporting line. An empowered CDO reports to the CEO, or to a Board committee with direct CEO access. A CDO reporting into the CTO becomes a sub-function of technology. A CDO reporting into the CRO becomes a sub-function of compliance. In both cases, data stops being a strategy and becomes a service. The organization reads this signal faster than any memo.

Budget authority and P&L influence. The ceremonial CDO controls a ring-fenced infrastructure budget. The empowered CDO allocates capital wherever data readiness determines strategic return, and influences the P&Ls of the business lines because he sits at the table when the bank decides which products to build, which segments to win, and how to price.

A genuinely cross-functional mandate. The typical CDO inherits a functional silo. The empowered CDO’s mandate cuts horizontally through every business line. He is present when credit policy is written, when wealth products are designed, when a new market is entered. He is not consulted after the decision. He is in the room before it.

Explicit decision rights. Empowerment requires the authority to say no. No to architectural choices that fragment the customer record. No to product launches that bypass data integration. No to AI pilots unsupported by model governance. These rights prevent the debt that slowly suffocates data ambition.

Cultural license to challenge. The hardest dimension to grant and the easiest to withdraw. The CDO must be visibly authorized to ask uncomfortable questions. Why do seventeen systems hold pieces of the same customer? Why are we segmenting by product when the customer’s life is not organized that way? Without cultural license, the CDO becomes a witness to institutional inertia rather than an agent against it.

A strong reporting line without budget authority is advisory theater. Budget without mandate is capital without direction. Decision rights without cultural license mean the CDO can block, but cannot lead.

All five must be present, and all five must be visibly reinforced by the CEO. Empowerment granted in private is not empowerment.

Why Now

Banks have operated for most of their modern history inside a benign envelope. Regulatory barriers discouraged entry, customer alternatives were limited, and the CDO role, where it existed, was a compliance footnote.

That envelope is tearing.

Banking is now a data industry. Supervisors and strategists treat financial services as an information business wrapped in a balance sheet, not the other way around. A bank that still treats data as plumbing is falling behind its own regulator.

Open Banking is rewriting competitive geometry. What was once a private moat becomes a shared reservoir. The winners segment faster, personalize deeper, and move from insight to product more quickly than the fintechs circling their customer base.

Fintechs and neobanks carry none of the legacy that incumbents do. No twenty-year-old core. No fragmented customer record. An incumbent without an empowered CDO is trying to win a sprint wearing ankle weights.

Customer expectations have been reset by adjacent industries. People no longer benchmark their bank against other banks. They benchmark it against every digital experience they have.

Generative AI has compressed the strategic horizon. What was a five-year roadmap two years ago is an eighteen-month imperative today. The gap between banks that deploy these capabilities responsibly and those that cannot is widening faster than planning cycles can absorb.

Regulatory modernization is no longer incremental. A bank’s ability to respond at regulatory speed is now a function of its data architecture, not its legal department.

Built well, the CDO role becomes the operating lever for everything above. Built poorly, it becomes the excuse for why none of it worked. The middle ground has disappeared.

The Six Shifts an Empowered CDO Unlocks

- From Reporting to Revenue. The traditional data function looks backward because the monthly close demands it. An empowered CDO asks a different question: what does the bank know about its customers that no competitor can replicate, and how is it worth money? In credit, that turns decisioning from a bottleneck into a relationship event. In wealth, a decade of transactional history becomes the raw material of a 360-degree financial portrait no external advisor can assemble. In commercial banking, it enables early-warning systems and real-time pricing that reflects the client’s current balance sheet, not last year’s file.

- From Reactive to Predictive Risk. Most bank risk functions are archaeologists. An empowered CDO reorients them toward anticipation. Credit exposure adjusts weeks before traditional review cycles would notice. AML retires rules-based systems that drown investigators in false positives and replaces them with probabilistic models. Fraud detection runs in milliseconds. Operational risk becomes forecast, not forensic.

The ceremonial CDO inherits yesterday’s data problems. The empowered CDO inherits tomorrow’s competitive advantage.

- From AI Ambition to AI Readiness. Every bank has an AI strategy. Few have the foundations to execute one. The pilot performs beautifully on curated data. Production reveals the data is fragmented across seventeen systems. An empowered CDO breaks this cycle by sequencing correctly: unified customer record, cleansed transaction layer, model governance that specifies how a model is tested, deployed, monitored, and retired. This work wins no awards. It is the difference between banks that deploy AI and banks that announce AI.

- From Product-Centric to Customer-Centric. Most banks know many things about their customers and understand none of them. An empowered CDO collapses the silos at the data layer, even when the org chart resists. A family with fifty million across four product lines is today, functionally, four customers. At a bank with an empowered CDO, it is one. The difference is not marginal. It is categorical.

- From Cost Center to Operational Alpha. Straight-through processing compresses cost per transaction by thirty percent while accelerating execution from days to hours. Branch footprints right-size with evidence rather than instinct. Collections become predictive. Regulatory reporting becomes automated rather than heroic. In a mature industry with thin margins, this is where competitive advantage is actually built.

- From Scarcity to Talent Magnetism. Banks lose the talent war when they treat data as back-office overhead. An empowered CDO changes the signal: data roles become visible, senior, and consequential. Over time, the bank builds the rarest asset in financial services, people who understand both sides of the problem.

A bank cannot win on capital and brand alone. It must win on speed, insight, and execution. Those are cultural outputs, not technical ones.

Why Empowerment Fails

The logic is persuasive. The execution is where most banks discover empowerment is harder to implement than to announce. The failure modes recur with uncomfortable predictability.

Unclear mandate. Boards appoint a CDO without agreeing on what success looks like. When the answer is “all of it,” the role has no center of gravity. A CDO paid on audit outcomes will optimize for audits, not transformation.

Cultural resistance. Empowerment requires existing executives to cede authority. The CTO loses architectural monopoly. The CRO shares ground on model governance. The CMO accepts that segmentation is no longer a marketing prerogative. Passive resistance is the most common response: authority on paper, obstruction in practice. The CEO eventually loses patience with the appointment, not with the system that strangled it.

Legacy technology debt. Modern analytics cannot be built on a twenty-year-old core without repair. That repair is expensive, politically fraught, and often deferred. The CDO is left trying to build the future on top of the past, and cannot win that fight alone.

Short tenures. Data transformation produces results on a four-to-five-year horizon. Many banks treat the CDO role as a two-year rotation. A CDO who knows he will be gone before the payoff arrives optimizes for visible short-term wins and avoids the difficult decisions that require political capital he will never get to spend.

The scapegoat trap. When mandates are unclear and resistance is quiet, the CDO becomes the institutional explanation for failure. The role becomes a rationalization for inaction rather than a catalyst for action.

The remedy is exacting. Clarify the mandate before the appointment. Make CEO support visible and repeated. Align incentives with strategic outcomes. Commit to a tenure that matches the work. Budget for technical debt honestly. Without these guardrails, empowerment is theater, and everyone in the building eventually figures it out.

The Board’s Playbook: RAISE

For CEOs and Boards prepared to move from appointment to empowerment, the work organizes into five actions.

R — Reporting. A direct line from the CDO to the CEO, with standing presence at the Board’s Risk or Transformation Committee, and full-Board presentations at least twice yearly.

A — Authority. Explicit decision rights across data architecture, governance policy, data product initiatives, enterprise AI and model governance, and data-related organizational design. Escalation paths defined in advance.

I — Integration. The CDO embedded in every cross-functional leadership forum where consequential decisions are made. A monthly data council chaired by the CDO, where data considerations enter decisions, not where they arrive afterward.

S — Stewardship. Success defined in outcome terms: customer value, operational efficiency, risk posture, regulatory readiness. Reviewed quarterly. Delivery rewarded visibly. The role never allowed to drift into symbolism.

E — Enablement. The work funded honestly. A multi-year investment plan defended against the predictable pressure to cut.

None of this is unusual for how modern organizations empower a strategic function. What is unusual is how rarely it is applied to the CDO.

The Bank in 2030

Imagine, six years from now, a bank that made the turn.

Its CDO is a strategic partner to the CEO, consulted before market entries, product launches, and M&A. Customer experience no longer feels like a series of disconnected transactions. Credit decisions are instantaneous and explainable. Regulatory reporting is a by-product of operations, not a parallel industrial process. Risk is anticipatory: stress caught before it becomes loss, fraud blocked before it becomes disputed. When a customer segment begins to defect, the bank sees it in weeks rather than in the next annual review.

And the talent follows. Engineers and analysts who would once have left for technology firms see a credible future inside the institution.

None of this is fantasy. It is the baseline being built today by a small number of global leaders, and the gap between them and everyone else is widening. The question is not whether the model works. The question is which banks will have built it by the time Open Banking matures, AI governance hardens, and the next generation of competitors forces the issue.

In a sector where data has become the currency of competition, risk, and strategy, an unempowered CDO is a slow-motion strategic error.

The window is open. It is not wide. The banks that act will build institutions that lead the next decade. The banks that hesitate will spend it explaining, in increasingly defensive language, why the transformation took longer than expected.

The appointment was the easy part. The empowerment is the job.